As focus shifts from lifespan to health span, a real question emerges: will value remain fragmented across well-capitalized point solutions, or concentrate in a handful of platforms that specialize in personalizing medicine across women’s life stages?

A familiar pattern in health innovation is accelerating the longevity movement, shifting care from episodic intervention to longitudinal management. We’re seeing the promise of prevention and personalization, enabled by better measurement — at-home tests, continuous signals, biomarkers, “bio-age,” and dashboards that let people track their physiology directly.

But this pattern also risks a major blind spot in women’s health when platforms aren’t built fit for purpose, and when women’s health is treated as a category market rather than a biological system. When it comes to longevity, women’s health is not an edge-case participant, but its central driver — and the proving ground for if longevity platforms can actually work at scale.

Why?

- Women live longer than men, yet spend more years in poorer health.

- Ovaries are the fastest aging organ, yet among the least studied in aging research; most longevity science is built on male models & data

- And yet, across many species, females tend to age more slowly, with biological features (e.g., estrogen-mediated effects) that could hold underexplored clues to aging insights

If longevity models can’t make sense of women’s biology, they’re unlikely to work for everyone.

Women’s health exposes the boundaries of what’s real in longevity. Consumer platforms are increasingly promising answers that healthcare itself doesn’t yet have. Nowhere is that tension more apparent than in women’s health, where foundational biological gaps persist across life stages, but especially in mid- to late life: menopause, migraines, Alzheimer’s, heart disease, and autoimmune conditions. As long as those gaps remain, this market must face a difficult question: can it mature into real healthcare at scale without overpromising, or losing what made it appealing in the first place?

For decades, women’s health was packaged as moments across aisles: contraception, pregnancy tests, menopause supplements. While great brands can exist in those moments, women don’t experience their health in neatly packaged moments. They experience it continuously, combinatorially, often through complex life transitions, with noisy, cyclical signals and questions that don’t fit into a ten-minute appointment: Is this normal? What’s changing?

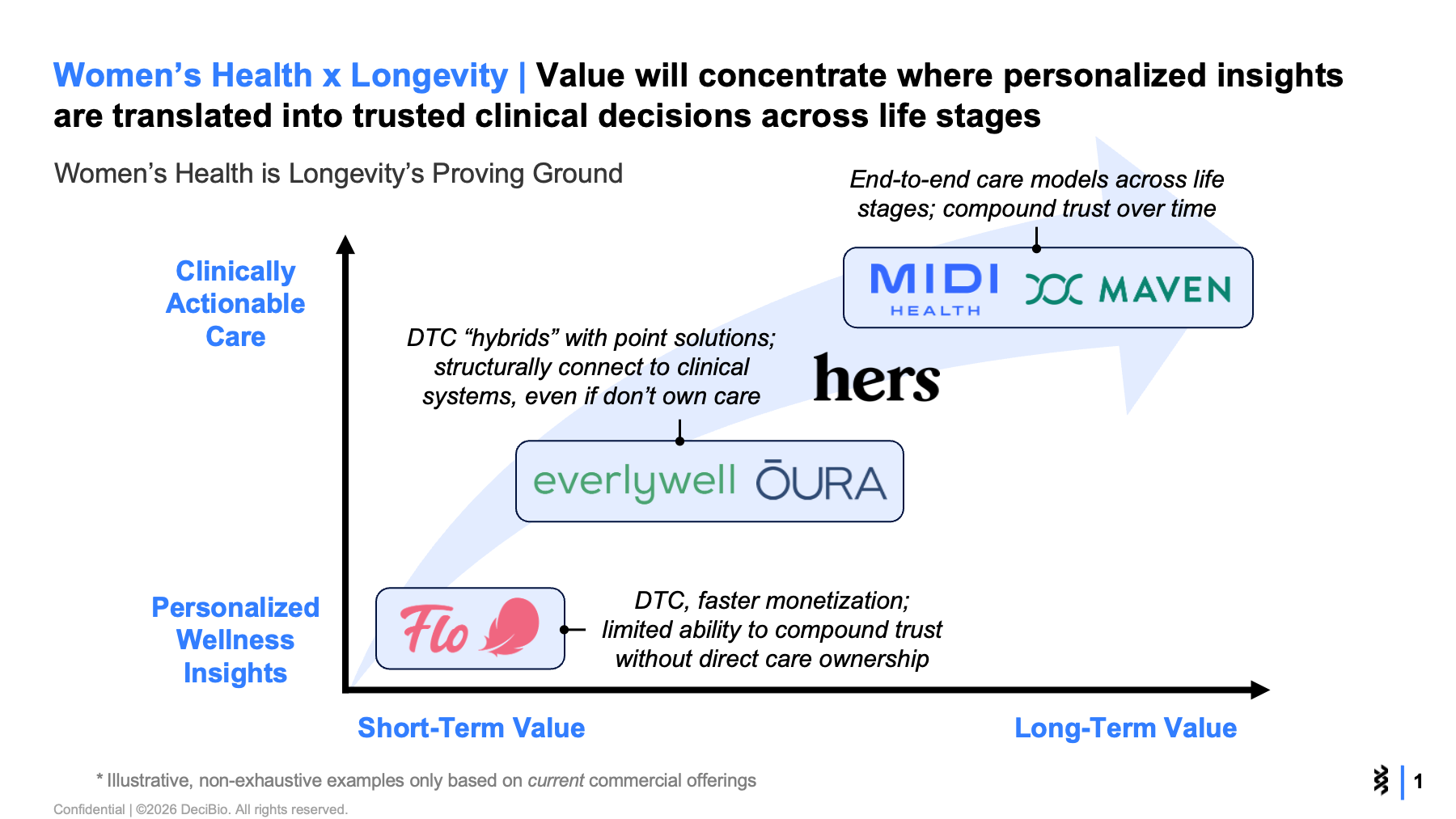

This is where women’s health becomes the blueprint for longevity platforms — if, and this is a big if, it can move beyond a collection of measurements packaged under an AI algorithm. The most valuable pillar to prevention is not measurement itself, but what it unlocks downstream: interpretation, a plan, follow-through, and escalation when needed. Not an app or supplement. Not partial disjointed answers scattered across “moments.” An end-to end, closed care system.

You can see this shift in the strongest women’s health startups. Consider Midi Health, women’s health’s first menopause unicorn. Midi began by addressing a deeply personal problem that healthcare chronically underserved. It evolved from a telehealth product into a menopause-first clinical protocol, and then a longitudinal model built around transition and continuity. By expanding around menopause (e.g., sleep, mental health, preventive screening), Midi embraced the complexity that real-world women’s health doesn’t fit neatly into discrete specialties.

That’s the strategic unlock: women’s health is naturally uniquely suited to long-term, subscription-like relationships grounded in moments that surface as symptoms, decisions, and transitions: fertility planning, postpartum recovery, perimenopause, sleep disruption, libido changes, metabolic shifts. This is also why longevity, wellness, and even beauty are increasingly becoming hormone-aware. Hormones sit beneath much of today’s consumer health language: sleep, stress, metabolism, energy, mood recovery, resilience, etc. But today’s hormone awareness still lacks a structured, clinically actionable way to operationalize it.

Hormone-aware consumer health sits at an inflection point. It can either become a credible bridge between wellness and medicine, or the next Wild West of “personalized” marketing claims. Recent FDA guidance made one thing clear: the moment products imply disease risk or clinical decision-making, they move from lifestyle marketing into regulated medical territory. Personalization carries clinical responsibility; the moment a company tailors recommendations to an individual’s biology, it implicitly makes medical promises. Most “personalized health” today falls short. What’s marketed as personalization is often just insight: here’s your score. But action without guardrails (even implied) creates real risk, for both users and companies.

That risk is acutely apparent in women’s health because biological variability is a feature, not a bug. Hormone cycles create signal noise that breaks simplistic models. Symptoms can be very real even when standard labs look “normal.” When a company mishandles that uncertainty, the downside is asymmetric: done right, gains are typically modest and gradual; done wrong, customer trust can erode immediately and irreversibly. Reputational damage spreads faster than customer acquisition efforts — a particularly unforgiving margin-for-error for start-ups with limited capital and brand equity.

Long-term winners need more than fancy branding or dashboards. They must be able to clearly communicate uncertainty without eroding consumer trust. That could look like pairing hormonal insights with clinical rigor and pathways to care, and being able to say: Here’s what we can measure well. Here’s what we can’t. Here’s what’s low-risk. Here’s what’s experimental. Here’s when to escalate to a clinician. Here’s how we help you do that.

This runs counter to current market incentives. Marketing rewards clean stories, but biology is messy. Short term, well-capitalized, point-solution brands might win. But over time, the market will reward companies that reliably demonstrate that their speciality, not their marketing story, is personalization. The next wave will win by operationalizing personalization with follow-up care architecture, triage logic, escalation pathways, and explicit risk thresholds.

Women’s health could be one of the most powerful drivers of longevity outcomes, but it’s overlooked because it’s structurally harder. It’s easier to sell a personalization score with near-term ROI than to build a reliable care model for a complex life-stage transition. Easier to sell a point-solution than to own a closed loop. But over time, this difficulty will become the moat. In an increasingly saturated market, platforms will differentiate toward DTC-hybrids, blending software with services and consumer-grade experience with medical rigor.

So what does this mean today?

- Investors: underwrite platforms with long-term “hybrid” differentiation potential

- New entrants: resist temptation to stop at insights & engagement; build the closed loop

- Incumbents: recognize the game is changing; products without actionable outcomes won’t be enough anymore

- Healthcare systems: acknowledge that consumer health is becoming the front door to care and help ensure that happens safely; ultimately, their customers are your patients

Consumers are signaling they want a different contract with health, centered around prevention, continuity, and actionable interpretation over time. Platforms that can safely scale personalization across women’s life stages will realize that women’s health is more than just a niche in the future of the longevity movement — it is the greatest playground.

_______________________

Note: Some of the companies listed in this article may be DeciBio Consulting clients.

Connect with Mané on LinkedIn

.png)

.png)